PNB Gold Debit Card vs PNB RuPay PMJDY Debit Card Comparison – Fees, Rewards & Benefits Explained

Introduction

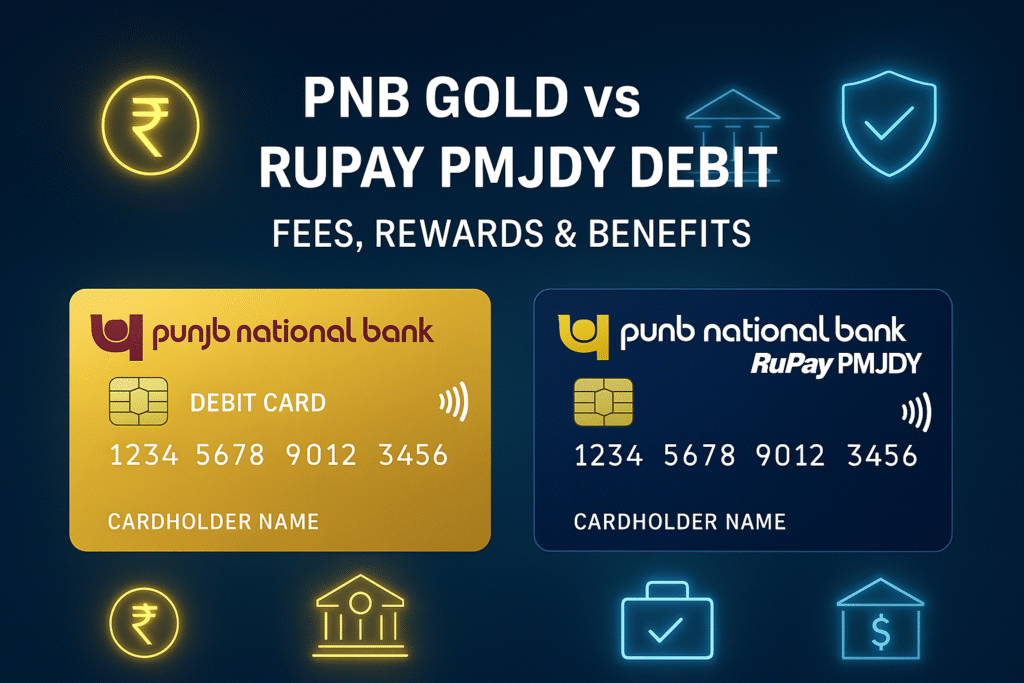

Punjab National Bank (PNB) is one of India’s leading public sector banks, offering debit cards for every type of customer—from first-time account holders to premium users seeking lifestyle benefits. Among the wide portfolio, two cards often compared are the PNB Gold Debit Card and the PNB RuPay PMJDY Debit Card.

The PNB Gold Debit Card is designed as a budget-friendly option with basic savings and rewards, making it suitable for regular salaried and middle-income users. The PNB RuPay PMJDY Debit Card, however, has been introduced under the Pradhan Mantri Jan Dhan Yojana (PMJDY), specifically aimed at financial inclusion. It allows unbanked citizens to access digital payments and basic financial services at little to no cost.

If you’re wondering “What’s the difference between the PNB Gold Debit Card and PNB RuPay PMJDY Debit Card?”, this blog will break down the fees, benefits, and usage features of both cards so you can understand which fits your needs in 2025.

1. Annual Fees and Charges

The PNB Gold Debit Card comes with a minimal joining fee and low annual charges. It is not free, but its fees are affordable, making it accessible to cost-conscious customers who want to enjoy small perks.

The PNB RuPay PMJDY Debit Card is designed for financial inclusion and usually has no joining fee and no annual maintenance charges. This makes it perfect for first-time account holders under Jan Dhan Yojana who may not want to pay for a card.

2. Rewards and Cashback Benefits

The PNB Gold Debit Card offers basic cashback and reward points on shopping, fuel, and online payments. While not very high, these benefits provide consistent savings for everyday users.

The PNB RuPay PMJDY Debit Card focuses less on rewards and more on usability. It generally does not provide cashback or premium offers, but it ensures access to digital payments, government subsidies, and DBT (Direct Benefit Transfers).

3. Insurance and Protection Benefits

The PNB Gold Debit Card comes with basic personal accident insurance coverage and limited protection against unauthorized transactions. It offers peace of mind for users with moderate spending needs.

The PNB RuPay PMJDY Debit Card offers government-backed accidental insurance coverage, often ranging up to ₹2 lakh, depending on usage and scheme updates. This makes it highly valuable for low-income users, ensuring safety in case of accidents.

4. International Usage

The PNB Gold Debit Card can be used internationally at ATMs and POS terminals, although with lower limits compared to premium cards. It is better suited for domestic use with occasional foreign transactions.

The PNB RuPay PMJDY Debit Card is primarily a domestic-use card. While RuPay Global partnerships have expanded acceptance abroad, this card is mainly focused on India-based transactions for inclusion purposes.

5. Ideal User Profile

The PNB Gold Debit Card is ideal for regular banking customers who want a low-cost card with some added benefits like cashback, online shopping convenience, and insurance.

The PNB RuPay PMJDY Debit Card is meant for first-time bank account holders under the Jan Dhan Yojana scheme. It focuses on financial inclusion, government benefit transfers, and providing banking access to rural and low-income families.

Conclusion

Both PNB Gold Debit Card and PNB RuPay PMJDY Debit Card are excellent in their respective categories. The Gold Debit Card is a practical choice for salaried individuals and everyday customers seeking rewards and basic benefits. The RuPay PMJDY Debit Card, however, plays a bigger role in financial inclusion, ensuring that every Indian citizen has access to banking and digital payments.

Your choice should depend on your lifestyle: everyday savings with Gold, or government benefits and inclusion with PMJDY.